Income Tax in India : Guide, IT Returns,

E-filing Process 2018

Taxes in India can be

categorized as direct and indirect

taxes. Direct tax is a tax you pay on your income directly to the

government. Indirect tax is a tax that somebody else collects on your behalf

and pays to the government eg restaurants, theatres and e-commerce websites

recover taxes from you on goods you purchase or a service you avail. This tax

is, in turn, passed down to the government. Direct

Taxes are broadly classified as :

- Income Tax – This is taxes an

individual or a Hindu Undivided Family or any taxpayer other than

companies, pay on the income received. The law prescribes the rate at

which such income should be taxed

- Corporate Tax – This is the tax

that companies pay on the profits they make from their businesses. Here

again, a specific rate of tax for corporates has been prescribed by the

income tax laws of India.

Indirect

taxes take many forms: service tax on restaurant bills and movie

tickets, value-added tax or VAT on goods such as clothes and electronics. Goods

and services tax, which has recently been introduced is a unified tax that has

replaced all the indirect taxes that business owners have to deal with.

|

31 January

|

31 March

|

31 July

|

Oct – Nov

|

|

Deadline to submit

your investment proofs

|

Deadline to make

investments under Section 80C

|

Last date to file

your tax return

|

Time to verify your

tax return

|

Income Tax Basics

Everyone

who earns or gets an income in India is subject to income tax. (Yes, be it a

resident or a non-resident of India ). Also read our article on Income Tax for NRIs. Your income could be

salary, pension or could be from a savings account that’s quietly accumulating

a 4% interest. Even, winners of ‘Kaun Banega Crorepati’ have to pay tax on

their prize money. For simpler classification, the Income Tax Department breaks

down income into five heads:

|

Head of Income

|

Nature of Income

covered

|

|

Income from Salary

|

Income from salary

and pension are covered under here

|

|

Income from Other

Sources

|

Income from savings

bank account interest, fixed deposits, winning KBC

|

|

Income from House

Property

|

This is rental

income mostly

|

|

Income from Capital

Gains

|

Income from sale of

a capital asset such as mutual funds, shares, house property

|

|

Income from

Business and Profession

|

This is when you

are self-employed, work as a freelancer or contractor, or you run a business.

Life insurance agents, chartered accountants, doctors and lawyers who have

their own practice, tuition teachers

|

Taxpayers and Income Tax

Slabs

Taxpayers in India, for

the purpose of income tax includes:

- Individuals, Hindu Undivided

Family (HUF), Association of Persons(AOP) and Body of Individuals (BOI)

- Firms

- Companies

Each of these taxpayers

is taxed differently under the Indian income tax laws. While firms and Indian

companies have a fixed rate of tax of 30% of profits, the individual,HUF, AOP

and BOI taxpayers are taxed based on the income slab they fall under. People’s

incomes are grouped into blocks called tax brackets or tax slabs. And each tax

slab has a different tax rate. In India, we have four tax brackets each with an

increasing tax rate.

- Income earners of up to 2.5 lakhs

- Income earners of between 2.5

lakhs and 5 lakhs

- Income earners of between 5 lakhs

and 10 lakhs

- Those earning more than Rs 10

lakhs

|

Income Range

|

Tax rate

|

Tax to be paid

|

|

Up to Rs.2,50,000

|

0

|

No tax

|

|

Between Rs 2.5

lakhs and Rs 5 lakhs

|

5%

|

5% of your taxable

income

|

|

Between Rs 5 lakhs

and Rs 10 lakhs

|

20%

|

Rs 12,500+ 20% of

income above Rs 5 lakhs

|

|

Above 10 lakhs

|

30%

|

Rs 1,12,500+ 30% of

income above Rs 10 lakhs

|

This is the income tax

slab for FY 2017-18 for taxpayers under 60 years. There are two other tax slabs

for two other age groups: those who are 60 and older and those who are above

80.

A word of note: People often misunderstand that if they earn let’s say Rs.12 lakhs, they will be paying a 30% tax on Rs.12 lakhs i.e Rs.3,60,000. That’s incorrect. A person earning 12 lakhs in the progressive tax system, will pay Rs.1,12,500+ Rs.60,000 = Rs. 1,72,500.

Check out the income tax slabs for previous years and other age brackets.

A word of note: People often misunderstand that if they earn let’s say Rs.12 lakhs, they will be paying a 30% tax on Rs.12 lakhs i.e Rs.3,60,000. That’s incorrect. A person earning 12 lakhs in the progressive tax system, will pay Rs.1,12,500+ Rs.60,000 = Rs. 1,72,500.

Check out the income tax slabs for previous years and other age brackets.

Exceptions to the Tax

Slab

One

must bear in mind that not all income can be taxed on slab basis. Capital gains

income is an exception to this rule. Capital gains are taxed depending on the

asset you own and how long you’ve had it. The holding period would determine if

an asset is long term or short term. The holding period to determine nature of

asset also differs for different assets. A quick glance of holding periods,

nature of asset and the rate of tax for each of them is given below.

|

Type of capital

asset

|

Holding period

|

Tax rate

|

|

Holding more than

24 months – Long Term Holding less than 24 months – Short Term

|

20% Depends on slab

rate

|

|

|

Debt mutual funds

|

Holding more than

36 months – Long Term Holding less than 36 months – Short Term

|

20% Depends on slab

rate

|

|

Equity mutual funds

|

Holding more than

12 months – Long Term Holding less than 12 months – Short Term

|

Exempt (until 31

March 2018) Gains > Rs 1 lakh taxable @ 10% 15%

|

|

Shares (STT paid)

|

Holding more than

12 months – Long Term Holding less than 12 months – Short Term

|

Exempt (until 31

March 2018)Gains > Rs 1 lakh taxable @ 10% 15%

|

|

Shares (STT unpaid)

|

Holding more than

12 months – Long Term Holding less than 12 months – Short Term

|

20% As per Slab

Rates

|

|

FMPs

|

Holding more than

36 months – Long Term Holding less than 36 months – Short Term

|

20% Depends on slab

rate

|

Residents and non residents:

Levy of income tax in

India is dependent on the residential status of a taxpayer. Individuals who

qualify as a resident in India must pay tax on their global income in India

i.e. income earned in India and abroad. Whereas, those who qualify as

Non-residents need to pay taxes only on their Indian income. The residential

status has to be determined separately for every financial year for which

income and taxes are computed.

Defining Income

Income has been very

widely defined in the Income-tax Act. In simple words, income includes salary,

pension, rental income, profits out of any business or profession, any profit

made out of the sale of any specified asset, interest income, dividends,

royalty income etc. The law classifies income under 5 major heads as already

mentioned above.

- Salary Income

- House Property income

- Profits and Gains from Business or

Profession

- Capital Gains

- Income from other Sources

The law also allows a

taxpayer to claim deductions specific to each such income and hence to avail

the appropriate deductions, it is important that you classify income under the

right heads. Eg. A salaried taxpayer can claim a standard deduction of Rs 40,000

while a taxpayer having rental income from a flat can claim municipal taxes as

a deduction.

Income Tax deductions

There are broad themes to

what the government incentivizes. These are either in the form of:

- Various deductions available under

Section 80 of the Income Tax Act which can be claimed from the Total

Income or

- Deductions that are specific to

each source of income.

Some of the key

deductions have been discussed here:

Home ownership

- Stamp duty and Registration under

Section 80C

- Home loan principal and interest

- First time homeowner benefit of

Rs.50,000 under Section 80EE

|

Deduction on

|

Maximum allowed

(for self-occupied house property)

|

Maximum allowed

(for property on rent)

|

|

Stamp duty and

registration + principal

|

Rs.1,50,000 within

the overall limit of Section 80C

|

Rs.1,50,000 within

the overall limit of Section 80C

|

|

Deduction on home

loan interest under Section 24

|

Rs.2,00,000

|

No cap (but rental

income must be shown in the income tax return) Further, maximum loss from

house property capped at Rs 2 lakhs

|

|

Deduction for

first-time homeowners under Section 80EE *certain conditions apply

|

Rs.50,000

|

–

|

Home renting

- House Rent Allowance or HRA (for

salaried only) Given how many Indians move cities for work, this is a

common allowance most salaried individuals can find in their payslips. If

you are renting an apartment, be sure to claim this in your tax return.

- Section 80GG (if you are

renting and don’t get HRA) If

you are not salaried, or you are still salaried, but don’t get HRA, then

you can claim deduction for rent under Section 80GG. Learn more.

Health

- Life insurance premium under

Section 80C

- Medical insurance under Section

80D

- Preventative health checkups under

Section 80D

- Medical bills (for salaried only)(

replaced with standard deduction of Rs 40,000 effective 1 April 2018)

Tax

Deductions for health insurance under Section 80D in FY 2017-18

|

Person insured

|

Maximum deduction

Below 60 years

|

Maximum deduction

60 years or older

|

|

You, your spouse,

your children

|

Rs.25,000

|

Rs.50,000

|

|

Your parents

|

Rs.25,000

|

Rs.50,000

|

|

Preventative health

checkup

|

Rs.5,000

|

Rs.5,000

|

|

Maximum deduction

(includes preventative health checkup)

|

Rs.50,000

|

Rs.1,00,000

|

Long-term savings

Employee provident fund (for

salaried only)Companies cut 12% of your basic salary and put it in a fund

managed by EPFO.Public provident fundIndividuals can open a PPF account

from a post office or a public sector bank like State Bank of India and ICICI

Bank. All of these allow you a deduction under Section 80C upto RS 1.5 lakhs Contribution

to NPS is also another tax saving avenue for claim of deduction under Section

80CCD

Other investment avenues

|

Investment

|

Risk

|

Interest

|

Guaranteed Returns

|

Lock-in Period

|

|

ELSS funds

|

Equity-related risk

|

12-15% expected

|

No

|

3 years

|

|

NSC

|

Risk-free

|

7.6%

|

Yes

|

5 years

|

|

5-Year FDs

|

Risk-free

|

7-9% expected

|

Yes

|

5 years

|

Business profits

Running a business and

wondering how to go about your taxes? It is simple. Take your gross receipts

from your business and reduce various business related expenses from it eg

telephone, internet, salary you pay to people you have hired, depreciation on

the items that you use for your business like computer etc. What you are left

with are your profits that you need to offer as your Income

from Business. Similar is the method of computing your taxable profits if you

are carrying out a profession too. But make sure you maintain proper books of

accounts recording all your business transactions as law mandates that you do

do. However, if you do not want to maintain books, you may opt for Presumptive

taxation scheme where you will have to offer a fixed percentage of your gross

receipts as your income.

Tax Credits

Income of certain nature

will suffer a Tax Deduction at source itself. Eg salary, interest, rent,

commission etc. The person in charge of paying such income will have to

mandatorily deduct taxes before making the payment subject to certain

conditions. Similarly, one may be liable to pay advance taxes if taxes payable

after reducing TDS is Rs 10,000 or more. After TDS and advance tax, if there

still tax to be paid, the same would be paid in the form of Self Assessment

Taxes. All of the above taxes paid i.e. TDS, Advance Tax and Self Assessment

Tax would reflect in Form 26AS of the taxpayer which is a significant document

one needs to rely on while filing the return of income. This Form 26AS is

called the tax credit statement that contains all the tax credits lying against

you PAN for any given financial year.

Income Tax Rules

While the Income Tax Act,

1961 is the law enacted by the legislature for governing and administering

income taxes in India, Income Tax Rules, 1962 has been framed to help apply and

enforce the law contained in the Act. Further, the Rules cannot be read

independently. They must be read in conjunction with the Act only. Further, the

Rules must be within the framework of the Act and cannot override the

provisions of the Act. For example, the Act lays down the law with regard to

taxability of perquisites given by the employer to his employees as “salary”.

However, it does not discuss how the perquisites must be valued. Such valuation

is in turn prescribed under Rule 3 of the Income-tax Rules.

Income Tax Calculation

Every income that your

receive should form part of your income tax return. Of course, the law does

provide for exemption of certain incomes eg. dividend income from an Indian

company, LTCG on listed equity shares upto Rs 1 lakh in any financial year etc.

Therefore, here is a quick guideline you can probably follow to compute taxes

due on your income:

- List down all your income – be it

salary, rental income, capital gains, interest income or profits from your

business or profession

- Remove incomes that are exempt

under law

- Claim all applicable deductions

available under every source of income . eg claim standard deduction of Rs

40,000 from salary income, claim municipal taxes from rental income, claim

business related expenses from your business turnover etc

- Claim all applicable exemptions

under every head of income eg. amount reinvested in another house property

can be claimed as exemption from capital gains income etc

- Claim applicable deductions from

your total income eg the 80 deductions like 80C, 80D, 80TTA, 80TTB etc

- You will now arrive at your

taxable income. Check the tax slab you fall under and accordingly arrive

at your income tax payable.

The government keeps

introducing and altering tax slabs, schemes and tax benefits, so it’s a good

idea to keep up with the Budget.

Income Tax Payment

The Government collects

income tax from three channels:

- TDS

- Advance tax

- Self Assessment tax

TDS

- TDS exists to help government get

tax throughout the year. There’s a prescribed table on how much tax

deducted under what circumstances.

- Your employer cuts TDS based on

the information available to him about you. So if you’ve made investments,

but have not declared or if you live in a rented house, but have not

shared rent receipts, your finance department will have no choice but to

deduct tax based on only thing they know – your CTC.

- This is why the investment proofs

deadline in your office is super important. Save yourself some headache

and submit your investment proofs on time.

- Banks don’t know if you’re working

in a company or if income from fixed deposits is what you solely rely on.

So they deduct a standard 10% tax before they give away the interest. Now

if you fall in the 20% or 30% bracket, it’s on you to pay the remainder of

the income tax. That’s why sometimes you may find yourself paying some tax

at the time of filing a tax return.

- Make sure banks have your PAN

number. They deduct 20% tax if they don’t have your PAN in their records.

- Anyone who’s receiving an income

of a specified nature say salary, interest, commission, rent, professional

income etc. will have some percentage of tax withheld as prescribed by the

government.

Advance Tax

Self-employed

people must do the calculation themselves and pay the tax to the Government

periodically every quarter. The deadlines are:

|

Due Date

|

Advance Tax Payable

|

|

On or before 15th

June

|

15% of advance tax

|

|

On or before 15th

September

|

45% of advance tax

|

|

On or before 15th

December

|

75% of advance tax

|

|

On or before 15th

March

|

100% of advance tax

|

To calculate your advance

tax:

- Add up all the invoices received

and include future payments you will be receiving till March 31 to

estimate your taxable income.

- Deduct expenses directly related

to your business, and any investments you have made under Section 80C in

order to arrive at your taxable income.

- Determine your tax liability for

the year

- Reduce the Tax already deducted at

source from your tax liability as determined above

- If the remaining tax payable is

greater than Rs 10,000 you will have to pay advance taxes based on the

rates prescribed in the above table.

- Use the Income Tax Calculator to determine

your tax liability

Self Assessment Tax

When you are filing a tax

return and you find out that you need to pay additional tax, you’d be paying

self assessment tax. Another way to think about this would be.

- if you are paying tax for a

financial year after the deadline has ended, you will pay self assessment

tax.

- if you are paying tax for a

financial year during the financial year, you will pay advance tax.

Payment of TDS Advance

Tax and Self Assessment Tax:

TDS is deducted by the

payer himself and remitted to the government by him. Hence the taxpayer need

not worry about this part of his tax liability. As regards advance tax and self

assessment tax, the same can be discharged online using Challan 280. Read our

detailed guide on

payment of taxes online.

Income Tax Return

An Income Tax Return is a

form where a taxpayer discloses details of his income, claims applicable

deductions and exemptions and taxes that are payable on the taxable income.

Further, details of taxes paid also reflect in the return. Any excess tax paid

for a year will be claimed as a refund in the return of income.

Some taxpayers who are

into any business or profession disclose details of such business or profession

like turnover, expenses relating to business, profits from business etc. All

the above information, put together, form part of your return and is filed with

the Income Tax Department.

Income Tax Return Filing

Filing of income tax

return online has been made mandatory for all classes of taxpayers barring few

exceptions :

- Taxpayers aged 80 and above need

not filed return online

- Taxpayers having an income less

than Rs 5 lakhs and not claiming a refund need not file return online

Do note that deadlines

for filing of returns have also been prescribed. For most individual taxpayers,

the due date for filing return of income is 31 July immediately following the

concerned financial year. If you do not file on time, here are some

disadvantage:

- You will be denied carry forward of

losses (except house

property loss) to future years

- Delay processing of refund claims if any

- Difficulty on getting home loans

- Levy of late filing fee upto Rs

10,000 under Section 234F

- Levy of interest under 234A if

there are taxes due as on 31 July

E-filing online is a more

complete and better alternative to filing on the income tax website. Also it is

for more than just e-filing your income tax return. ClearTax helps you claim

all the deductions you’re eligible for and helps you invest.

Once you file your return

online, you either e-verify the same or take a print of the ITR V and send it

to CPC, bangalore for processing of your return. Read our detailed article on e-verification of return of income

ITR Forms

ITR forms i.e. the return

filing forms have been prescribed differently based on the class of taxpayers

and the source of income. See below for further clarity

Documents Required for

ITR Filing

Form 16, Form 26AS, Form

16A, proof of tax saving investments made, bank account details etc are some of

the crucial details / documents that you need to be ready with before filing

your return. Further the documents you are going to need to file your tax

return are largely going to depend on your source of income. Here is our

detailed article on documents you need for filing of your

return of income

Income Tax Faqs

- When it is mandatory to file

return of income ?

It is

mandatory to file return of income for a company and a firm. However,

individuals, HUF, AOP, BOI are mandatorily required to file return of income if

the income exceed basis exemption limit of Rs 2.5 lakhs. This limit is

different for senior citizens and super senior citizens.

- What are the maximum exemption

limit and slab rates applicable for Assessment Year 2018-19 ?

|

Income Slab

|

Resident and

non-resident individuals

|

Senior Citizens

(Above 60 yrs but less than 80 yrs)

|

Super Senior

Citizens (Above 80 yrs)

|

|

Upto Rs. 250,000

|

Nil

|

Nil

|

Nil

|

|

Rs. 250,001 – Rs.

300,000

|

5%

|

Nil

|

Nil

|

|

Rs. 300,001 – Rs.

500,000

|

5%

|

5%

|

Nil

|

|

Rs. 500,001 – Rs.

10,00,000

|

20%

|

20%

|

20%

|

|

Above Rs. 10,00,000

|

30%

|

30%

|

30%

|

- Can i file return of income even

if my income is below taxable limits ?

Yes,

you can file return of income voluntarily even if your income is less than

basic exemption limit

- What documents are to be enclosed

along the return of income?

There

is no need to enclose any documents with the return of income. However, one

should retain the documents to produce before any competent authority as and

when required in future.

- Should I disclose all my income in

the return even if it is exempt?

Yes.

Income from every source including exempt income must be disclosed. The same

can be shown under the Schedule EI.

Income Tax Tax Glossary

Form 26AS

Form 26AS is a tax

summary statement that contains all the tax payments you’ve made yourself

(self-assessment tax/ advance tax) or tax someone deducted (TDS) on your

behalf. You’re going to need this document when you are doing your income tax

e-filing. Form 26AS can be downloaded from www.incometaxindiaefiling.com

Form 16

If you need to know

whether or not your company has given you some tax allowance like your offer

letter says, or want to see how much tax has been deducted throughout the year,

or need to see EPF contributions, wouldn’t it be easier if you could see them

all in one place? That’s your Form 16. Form 16 has:

- a summary of all the tax deducted

by each quarter

- all the tax benefits and

allowances you’ve availed as a salaried individual

- Section 80C deductions you’ve

claimed through your employer

- and your taxable income after

allowances and Section 80C deductions

This is a super important

document for all salaried individuals. And having a Form 16 makes e-filing your

income tax return very simple. You can upload your Form 16 and e-file your

income tax return. No income tax login required.

Form 16A

Form 16A is very similar

to a Form 16 in that it contains how much tax was deducted over what income. So

how’s Form 16A different? Form 16A will never be issued by an employer. They’re

usually given to you by a bank that’s deducting TDS, or a company that’s

deducted tax on your freelancing service.

Investment submission proof deadline

Depending on how large

your company is, you might have two deadlines related to investment proofs.

There’s one in the beginning of the year (April) that needs you to just declare

how much money you’re planning to invest in Section 80C. This will give an

indication on how much they need to deduct in TDS.Again in the last quarter

(roughly between December and February), you will be asked to submit investment

proofs. This is when you need to submit all your rent receipts, medical bills

(if you’re getting medical reimbursement), investments under Section 80C, 80D.

Learn more about Investment submission

proof deadline

Assessment Year/ Financial Year

Financial Year runs

between April 1 and March 31 of each year. Income tax is calculated for this

period. Income tax returns are assessed the year after the financial year has

finished. So that’s your Assessment Year. During the assessment year, taxpayers

file their income tax return. Income tax return and refunds are processed by the

I-T Department that year.

ITR-V

ITRV stands for Income

Tax Return – Verification. After filing your tax return online, you must print

and sign a 1-page document and send it to the Income Tax Department.

Challan 280

Challan 280 is the slip

that you will use for online income tax payment. Follow this guide to learn how

to pay tax due. This

is the link to the

Income Tax Department website. If you are a taxpayer, you’re

going to need to use for:

- Getting your tax credit statement

Form 26AS

- Getting your tax records for home

loan or visa application

- Verifying your income tax return

after ITR submission

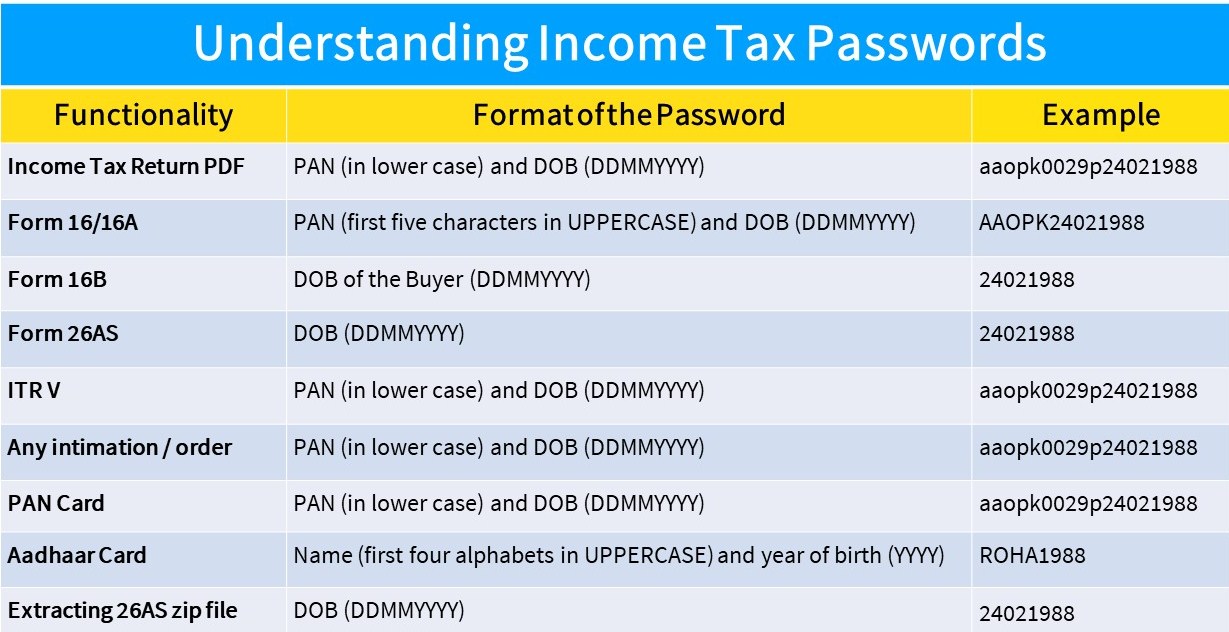

Important Passwords

Here we have listed the

most frequently downloaded documents and the format for the respective

passwords.

To understand the

application of these passwords better, let’s take an example

Rohan is a resident

individual who has been filing his tax returns for over ten years. His date of

birth is 24.02.1988. Rohan’s PAN is AAOPK0029P

Related

Income Tax Articles

No comments:

Post a Comment